When you hear talk about the Federal Reserve “cutting rates,” it can sound like a financial buzzword. However, the decisions made by the Federal Reserve to change the federal funds rate at which banks lend to each other, influences broader borrowing costs throughout the economy, including the interest rates on commercial real estate loans.

The 10-Year Treasury yield is one of the most widely watched indicators in finance as it reflects investor sentiment about the economy and inflation expectations. It’s a benchmark for various interest rates, including mortgage rates. As the yield rises or falls, these other rates often follow.

What is the Federal Reserve (“the Fed”)?

The Federal Reserve is the central bank of the United States, tasked with managing the country’s monetary policy. One of its primary responsibilities is to ensure the economy remains stable by balancing two main goals:

1. Maximizing employment

2. Keeping inflation in check (i.e., controlling rising prices).

What is the 10 Year Treasury Yield?

The 10-Year Treasury bond is a debt instrument issued by the U.S. government with a 10-year maturity, meaning investors are lending money to the government for a decade. Demand for Treasuries, driven by investor sentiment, plays a big role in determining bond prices and yields. The 10-Year Treasury serves as both:

1. An indicator for economic health

2. A benchmark for other rates (i.e., interest rates)

What Factors Influence the 10-Year Treasury Yield?

Economic conditions, inflation concerns, or Federal Reserve policy changes can drive prices up and yields down or vice versa. Rising yields can signal optimism about economic growth, while falling yields often reflect concerns about the economy or financial markets.

1. In times when inflation is expected to rise, yields often increase as investors demand higher returns to compensate for the erosion of purchasing power.

2. Interest rate decisions by the Federal Reserve affect yields by making bonds more or less attractive relative to other investments.

How Does the Fed Decide on Rate Cuts?

The Federal Reserve has a committee called the Federal Open Market Committee (FOMC), which meets eight times a year to review economic data and decide whether to raise, lower, or keep interest rates the same.

1. In times of economic slowdown, the Fed may decide to cut rates to make borrowing cheaper, encouraging more borrowing and spending to help stimulate the economy.

2. In times of economic crisis the Fed may aggressively cut rates to try to prevent a deep recession.

When Does the Fed Meet?

The FOMC meets about every six weeks, and dates are published on the Fed’s website. In 2024, for instance, the final calendar meeting is set to occur on December 17 and 18. Their decisions are usually announced in a statement following each meeting.

1. The 12 members, which include the seven members of the Federal Reserve Board and five of the 12 Reserve Bank presidents, discuss their findings and vote on whether to adjust the federal funds rate.

2. Post-meeting the Fed announces its decision, and the Chair of the Federal Reserve (Jerome Powell) holds a press conference explaining the reasoning behind the move.

In a Reuters poll from September 10, 2024, 100% of the more than 100 economists surveyed anticipated a rate cut announcement on September 18.

Nearly 70% predicted two more 25-basis-point rate cuts in 2024, after the FOMC meetings on November 6 and 7 and December 17 and 18.

What Do these Financial Instruments Mean for You?

Rate cuts and the 10-Year Treasury have direct and indirect effects on the everyday consumer. Investors use the 10-year yield as a signal for economic cycles and as a gauge for equity market movements. Here’s how they can impact commercial real estate:

1. Lower Loan Rates: When the Fed cuts rates, banks typically lower interest rates on loans making debt cheaper to finance or refinance big purchases. Speculation is that impact on CRE Loans was largely (not entirely) baked in over the last 30-45 days.

2. Mortgage Rate Predictor: Falling yields often lead to lower borrowing costs.

3. Savings Interest: Lower interest rates also mean that the return on savings accounts and certificates of deposit (CDs) might decrease. While it becomes cheaper to borrow, it becomes less lucrative to save in interest-bearing accounts and many turn to or turn back to commercial real estate.

4. Impact on CAP Rates: Capitalization rates in commercial real estate are expected to respond to interest rate cuts overtime – long-term yields are most influential. According to CBRE Econometric Advisors, CAP rates have shown varying degrees of sensitivity to changes in the 10-Year Treasury yield

Looking Ahead: Rate Cuts beyond 2024

The 75bps rate cuts are going to help move properties that weren’t selling before and bring more capital/buyers into the market. Strategists believe that there will likely be one additional rate cut in 2024 and expect the cuts to continue into 2025. There is more optimism in the market that we now have a path forward to seeing 5-5.5% loans again. Many see this as an opportunity to lock in attractive interest rates and consider a move out of excess cash positions.

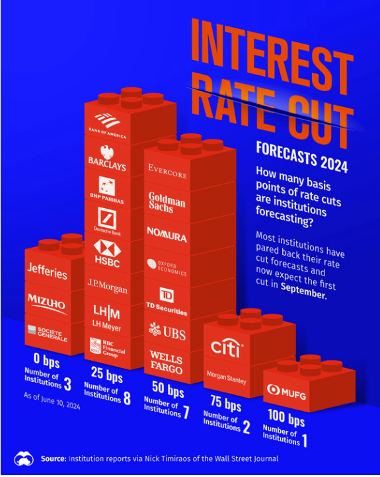

The magnitude of rate cuts being forecasted by major institutions earlier this year is shown here:

Conclusion

It goes to show that no one has a crystal ball. If you’re considering investing in commercial real estate, keeping an eye on rate cuts is insightful. The fed can influence borrowing costs which impact investment returns, making them a critical factor in personal and business financial planning. Maybe more importantly, due to its broad impact on borrowing costs, investment strategies, and economic indicators, watch the trends and shifts in the 10-Year Treasury Yield and what’s causing them.